The self-employed used to say that 401(k) plans weren’t in tune with their needs - but thanks to the 2001 federal tax act, they now are singing their praises.

Until the passage of the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) it didn’t make sense for the self-employed to establish 401(k) plans. Small-business owners could sometimes save just as much through a Keogh, SEP or SIMPLE IRA-without the costly setup and maintenance fees, complex rules, and burdensome administration associated with 401(k) plans.

Owner-Only Businesses

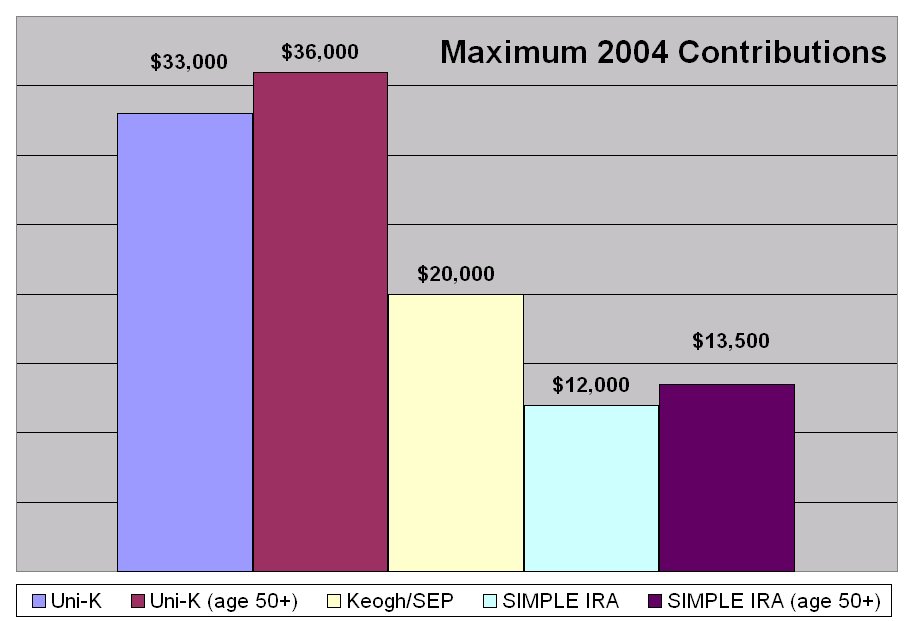

Owner-only businesses can now establish solo 401(k) plans that in some cases allow them to put away two to three times the amount allowed by other tax-deferred plans. Here’s an example of how this new, simplified retirement option stacks up against the competition:

Elizabeth owns an unincorporated business and has self-employment income of $100,000. By establishing a solo 401(k), also known as a “Uni-K”, she can put away as much as $32,000 in 2003-or $34,000 if age 50 or older. This total amount is tax deductible and all earnings grow tax-deferred until withdrawn.

How does this compare with the maximum deductible contributions allowed under other plans in 2003? It surpasses them all. Keogh and SEPs max out at $20,000, and the SIMPLE IRA at $11,000 ($12,000 if age 50 or older).

How It Works

The Uni-K contribution totals include employer and salary deferral contributions. If your business is incorporated, the employer contribution is based on your W-2 income and is capped at 25% of compensation. It is not subject to federal income tax or Social Security (FICA) taxes. The salary deferral contributions are withheld from your pay and are excluded from federal income tax, but are subject to FICA. The maximum salary deferral amount for 2003 is 100% of pay up to $12,000-or $14,000 if you are age 50 or older. Your business receives a tax deduction for both employer and salary deferral contributions. Employer contributions plus salary deferral contributions cannot exceed $40,000 ($42,000 if age 50 or older) or 100% of compensation.

Flexible, Uncomplicated, Accessible

The Uni-K has many benefits beyond its generous contribution limits. Consider the following:

- You decide each year whether to contribute and how much to contribute.

- Unlike traditional 401(k) plans, there are no complicated discrimination tests or administrative requirements. Among the few administrative requirements is an IRS Form 5500 filing-but only after plan assets exceed $100,000.

- You can take loans tax-free and penalty-free-under the same guidelines available to large corporate 401(k) plans.

- Retirement assets from other plans can be consolidated to create one convenient, low-cost account.

Business Owners and Spouses

This new planning opportunity is available to any business that employs only owners and their spouses, including C corporations, S corporations, partnerships and sole proprietorships. It is not suitable for businesses with employees, or those that plan to hire additional employees in the future.

Is a Uni-K right for you? If you’re a real estate broker, lawyer, accountant, electrician, or a member of one of the dozens of other self-employed professions, you owe it to your future to explore the advantages of a Uni-K.

(13680-00-0503) © Pioneer Funds Distributor, Inc. Underwriter of Pioneer mutual funds, Member SIPC